How is buying real estate in France? What’s the process? Is it too complicated? Is it a good idea? Pitfalls to avoid? Taxes?

We will be sharing in the key points on this topic based in our experience while living as expats in France.

Table of Contents

Buying or renting in real estate in France?

Deciding whether to buy or rent a property in France is a big decision, especially if you’re an expat who’s new to the country.

There are pros and cons to both options, and it’s important to consider your individual circumstances and preferences before making a decision. Here are the top 10 things to consider:

Your financial situation

In France, banks will apply the 1/3 rule to calculate the loan amount that you can afford. It means that they will grant you a loan if your monthly payment represents less than 1/3 of your total income. This is a very important rule to bear in mind when buying real estate in France.

As example, if you salary is 1000€, the max. amount of you monthly loan payment must not be higher than 330€.

The credit score in France works different as other countries (like USA) where the more you request and paid your credit cards, the better your score and better your loan rate. There is a credit track, which is more a kind of black list where people not paying their previous debt could be tracked but no influence in your rate.

Your length of stay

If you’re planning on staying in France for a short period of time, renting might be the better option than buying real estate in France.

However, if you’re planning on staying for a longer period of time, buying a property could be a good investment. As a general rule, you may consider a holding period of minimum 6 years to cover buying fees (like notary, real estate agency commission, etc.). If you are planning to stay less than that, you may want to rent instead.

myFrenchMoney tip

In order to make a data-driven desicion, we like a lot the Meilleurs Agents' calculator. It is in French, but you can use a digital translator and provide all relevant data to determine the breakeven time to live in your own property or if it is better to rent instead. Click on the green start to open it!

Your lifestyle

Consider your lifestyle and how owning or renting will fit into it. If you’re looking for more flexibility and the ability to move around frequently, renting may be a better option. If you’re looking for stability and the ability to make changes to your home as you see fit, owning may be a better option.

In France, you can rent a property ‘meublée’ (with furniture) or empty. First one will give you (and the landlord) more flexibility and you can receive a 3 month notice to leave the property. When rented empty, the notice period is 6 month.

Location

Location is always important when it comes to buying real estate in France. Consider the area you want to live in, the availability of rental properties or homes for sale, and the cost of living in that area.

Living in downtown Paris (an other major cities) is lots of fun, close to restaurants, museums, etc. You have access to everything in a 15m walk (no need of a car) but it could be noisy, small, polluted and very expensive.

In the other hand, avoid buying in bad neighborhoods, even if the property is super cheap. Remember, you can improve the property, but you cannot improve the location!

Maintenance and upkeep

When buying a property, you’ll be responsible for maintaining and repairing it. Renting, on the other hand, means that these responsibilities fall to the landlord. Are you willing and able to take on these responsibilities?

Unfortunately, it is more common to have some tenants late on payments, so you may want to ask a real estate agency to manage your property and subscribe to special assurance. Even if it will add additional cost to your investment (around 7%), you will gain peace of mind.

Finally, remember that buildings in France could be very old. In Paris, a 150 years old building is common. This implies high maintenance costs, like the famous ‘ravalement’ (front face restoration) that could represent some thousands of euros from your budget.

The French property market

The French property market is constantly changing, and it’s important to stay up to date on the latest trends and prices when buying real estate in France. It will help you make an informed decision about whether to buy or rent.

You can check by yourself the latest transactions from ‘notaires‘ even on your same building. This will give you a good idea of the local prices.

Your long-term goals

Consider your long-term goals and how owning or renting fits into them. If you’re looking to build wealth and establish roots in France, owning a property might be a good choice.

In opposite, if you’re looking for more flexibility and don’t want to be tied down to one place, renting might be a better option.

Interest rates

Interest rates. Interest rates in France can have a big impact on the cost of buying a property. Consider the current interest rates and how they might affect your decision. Interest rates in France are fix. It could be a good thing as it provides visibility on your budget.

Be aware that If rates comes down, you will be able to renegotiate it (worth it if >1% gap due to the fees). Here an article on how to negotiate a mortgage in France.

Taxes and fees

Buying a property in France comes with a variety of taxes and fees, including notaire fees (around 6% of property value), stamp duty, and important property taxes. These can add up quickly, so make sure you understand all the costs involved.

The French legal system

Finally, it’s important to understand the French legal system and how it applies to real estate. Working with a real estate agent or lawyer who speaks your language can help you navigate the legal aspects of buying or renting a property in France. Contact us if you want to get in contact with an English speaker realtor.

Investing in rental real estate in France

LMNP (with furniture) rental

There are many rental types in France, but there are 2 popular alternatives. The 1st one is called LMNP (‘Location Meublé Non Professionnel’) LMNP means that you are renting an apartment with minimum furniture so a person can live within.

There are well defined conditions about the type and number of furniture that you will need to provide to your tenant if you want to apply to this rental type. Typically you will need to include a bed, fridge, kitchen, etc.

Renting with a LMNP status is way more convenient in terms of flexibility and taxes. Here more details on the conditions and benefits.

Empty (no furniture) rental

An alternative option is to rent without any furniture ‘Nue propriété’ or empty. It is simpler, but you may struggle to find tenants, as it requires moving or buying the furniture and appliances.

Additionally, you will have less flexibility (in case you want to change tenant or sell your property) and less tax advantages.

The good side of it, is that the tenants tend to stay longer, compared to furnitured appartments.

General considerations

Regardless of the type you choose, having an apartment rented protects your investment from inflation as it is indexed to it. Meaning that you can raise your rent to your tenant every year but it is limited to 3,5% max.

Average rental investment’s return is around 3,6% for Paris and up to 5,2% in Montpellier. Yes, you can get more if short term rentals (like Airbnb). You should think twice for rental returns more than 5% as probably the risk is higher.

Finally, a key point to consider when investing in French real estate market is that mortgage interest rates are fixed but negotiable! If in few years from now interest rates drops, you can negotiate it with your bank (Learn more about how to negotiate a mortgage).

You may pay a fee but it will be few hundreds euros compared to thousands in interest savings. Normally the gap should be more than 1% to get some real savings.

myFrenchMoney tip

We like this web site https://horiz.io/rendement-locatif as it can help you calculating your return of investment. We love their web plugin to get the data right into your screen while surfing any web site.

Pitfalls to avoid while investing in rental real estate in France

Looking only for a high rental return rate

Not foreseeing unexpected costs

Do not forget the ‘taxe foncière’, high charges from the ‘co-propieté’ and any special work that may pop up.

Wrong cash flow calculation

Remember, be conservative with incomes and optimist with expenses estimations!

Investing in real estate for short term

Taxes when buying real estate in France

Income tax

Taxes will have a huge impact in your investment. French government taxes a lot this kind on investment to encourage citizen to put their money in other areas such as stock market but french love investing in ‘la pierre’ as it gives a security feeling compared to stock market.

By consequence, landlords are taxed as per their personal tax – TMI – tax bracket (could be up to 45%) + the social taxes 17,2% when renting a property.

In case you decide to sell your property, there will be a capital gains tax of 36,2% (depending on the holding time). You will need to keep the property for more then 30 years to be exempted from this tax.

Tax foncière

In addition to income tax, you will need to pay the ‘Taxe Foncière’ which could represent in some cases up to 1 months of rent. This amount depends on the city where the property is located.

This tax is to cover common expenses from the city like street cleaning, roads, parks, etc. You pay it once a year, around October, and it applies any property you own.

IFI Fortune tax

Then you have the ‘IFI Impôts sur les Fortunes Immobilières’. This is a tax if your total real estate net worth is more than +1,3M€. Certain rules applies to make the net evaluation of each property. Visit government site for more details.

French government has pass some laws to encourage citizens investing in real estate through tax advantaged conditions, such as ‘Loi Pinel’ but it will last till end 2024. Here our blog to learn more about taxes in France.

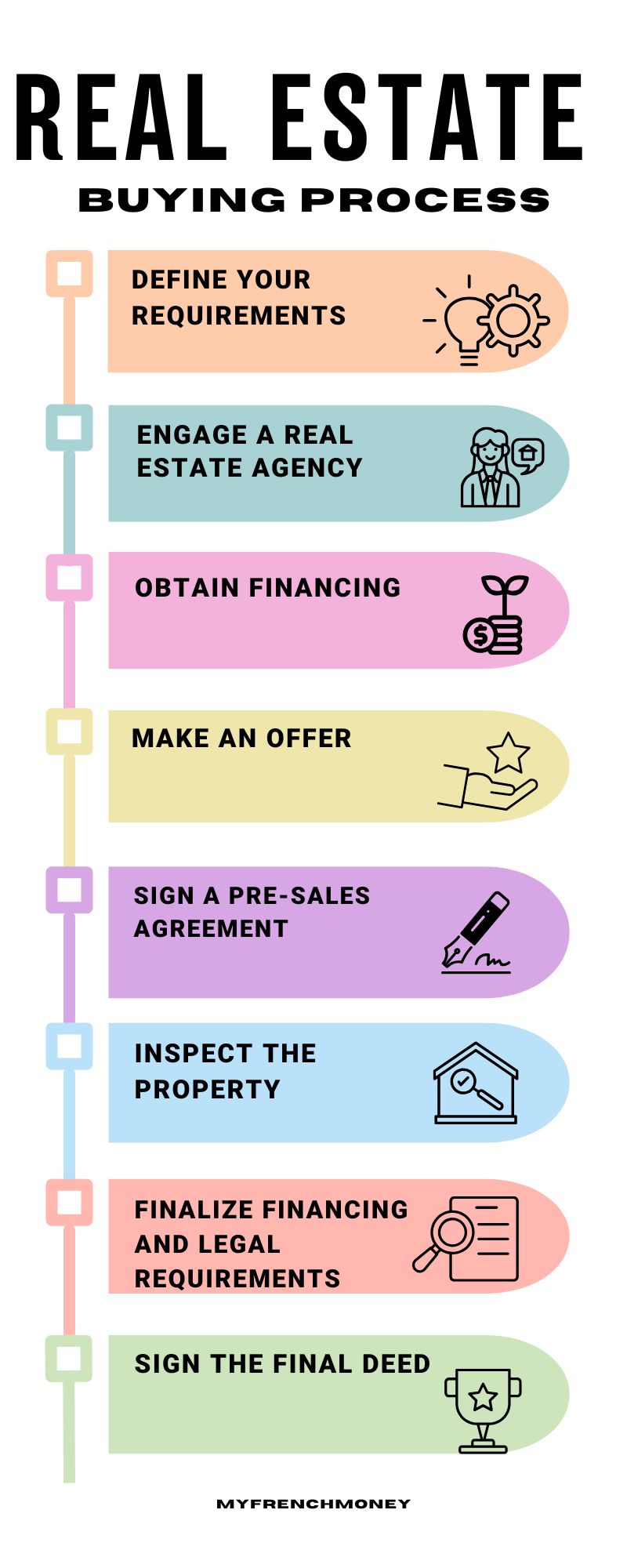

What is the process when buying real estate in France?

The process when buying real estate in France may vary depending on individual circumstances and the specific property. It is advisable to seek professional advice from an estate agent and a notary when buying property in France. Having said that, these are typically the common steps:

Define your requirements and research

Define your requirements and research: Start by defining your budget and search criteria (neighborhood, size, etc.). Perform a research online to finetune your requirements.

Engage a real estate agency

Once you find a property you are interested in, engage the services of a local estate agent who can guide you through the process. They can arrange property viewings and negotiate on your behalf. Bear in mind that best deals are not published to everybody in internet. The best is to have a realtor contacting you first!

Obtain financing

If you require financing, you should contact French banks or mortgage brokers to explore your options. It is advisable to get pre-approved for a mortgage before proceeding further.

Agency will give you priority if you have this buckled up. Here our blog about negotiating a mortgage.

Make an offer

Once you have found the property you want to buy, you can make an offer to the seller through your estate agent. If your offer is accepted, you will move forward to the next steps. In France you can propose a lower price as long as you can justify it (ex: property requires works).

Sign a preliminary sales agreement

It is known as ‘compromis de vente’. Both the buyer and seller sign a preliminary sales agreement, which outlines the terms and conditions of the sale, the purchase price, and any conditions or contingencies.

At this stage, you will typically pay a deposit of around 5% to 10% of the purchase price. There could be penalties if you do not honor the agreement.

Conduct property inspections

It is recommended to have a professional inspection of the property to identify any potential issues or defects. Visit the property as well during different time of the day and week. You do not want to learn the 1st night you move in that you have noisy neighbors 😉

You can request the support an expert (for a fee) to avoid discovering hidden or technical issues.

Finalize financing and legal requirement

If you are obtaining a mortgage, you will need to finalize the financing arrangements and provide the necessary documentation to the bank. If by any chance, you do not get the final bank agreement, you can break the deal with no penalties.

You will need to engage a notary, who is a public officer responsible for handling the legal aspects of the sale. The notary will conduct various searches and checks on the property, such as checking for liens or legal restrictions.

Sign the final deed

This is called in France ‘acte de vente’. Once all the legal requirements are fulfilled, you will sign the final deed of sale with the notary. At this stage, you will pay the remaining balance, including taxes and notary fees. After signing, the changes in ownership will be officially registered.

Transfer of ownership and taxes

The notary will handle the transfer of ownership and the payment of relevant taxes, such as the transfer tax (droits de mutation). The property will be officially registered under your name.

Our own experience

Buying our home

1st : an small old studio

We have changed home twice while living in Paris. Our first experience was totally different than the second. When we bought our first apartment we learnt the process, and how important is investing in real estate in France.

We have noticed that prices vary significative from one street to the other, or even in the same building but different floor. Parisians love sunlight and will be ready to pay more for just 1 floor higher. After COVID, having a balcony is a big plus.

Doing yourself the required works in your property can make you save a lot of money and important increase its value. We painted ourselves the studio (from yellow to super bright white) and remove some curtains to let sunlight going through. Thanks to this work we increased the value up to 5%.

When we decided to sell the studio, it took just few days to find a buyer. In Paris selling small apartments goes super fast as the demand is very high.

2nd: a bigger brand new apartment

Our second home, was bigger and in a new construction (rare inside Paris). It does not have the charm of ‘Haussmannian’ style but we’ve got comfort in return. The price was around 10% more expensive than old buildings thought. But the floor does not crack and we have a big elevator 😉

When buying a property in ‘état future d’achèvement’ (in blueprints), the conditions are different compared to an existing property. Delays and construction defects are common as well. We have got our apartment with 6 month delay and many things to fix. Not an easy process.

We are still living in this apartment … and we love it.

Rental investment

The investment consisted in a new apartment to get tax benefits as per the ‘Loi Pinel‘ conditions in Paris suburbs (back in 2018). We were not keen to invest in unfamiliar far-away locations and we were looking for a potential property value increase. We bought the apartment in blueprints (VEFA: Vente état future d’achévement’).

Good side

- Increase in our gross wealth. Investing in real estate in France has enable us to a significative increase our gross wealth thanks to the ‘leverage effect’. In few words, it is one of the rare (if not the only) financial asset in France (and many other countries) allowing individuals to invest with credit (getting richer with the bank’s money) while diversifying your portfolio.

- Low interest rate. We’ve got a great 1% mortgage rate and max-out our debt limit (35% of our total income). Here our blog with more details on how to negotiate a mortgage in France.

- Good tenant. So far, we have been luck with our tenant who’s the same since 2019. This is the pure merit from the agency managing our property (importance of good selection process).

- Tax benefits. We receive 6000€ back every year from our tax return (Loi Pinel main advantage) thanks to this investment.

Not so good side

- High initial effort. It took time to select the right property and dealing with paperwork. Once we’ve got the apartment, we had to install a kitchen to be able to compete with other apartments being rented at the same time than ours. We hired an agency to manage it. Finally after 3 months, we found a good tenant who’s still there since then.

- Potential limited capital gains. We fear that when the ‘Loi Pinel’ term comes to an end (2025), it will be the same case to many other apartments at the same building. If we want to sell, there could be more offer than demand.

myFrenchMoney final tip : avoid home oversizing!

Final words

If you found this blog useful, please share it with friends and follow us in LinkedIn to receive more content like this. You can leave your comments below or contact us in case of any further question.

Bon chance!

Disclaimer

Please remember that we are neither financial nor tax advisors nor real estate agents. We are just sharing our best understanding based in our own experience. This blog is for educational purposes only. Do not make investment decisions solely based on what you read in this blog. What works for us, may not for you. Do your own research and look for professional service if required. Read our full disclaimer in the ‘about’ page.