Table of Contents

You may have heard about SCPIs in France and wondered what they are all about. What does SCPI stand for? Is it a worthwhile investment? Why are they so popular in France? In this blog, we will answer all these questions and provide you with a comprehensive understanding of SCPIs and their appeal in the French investment landscape.

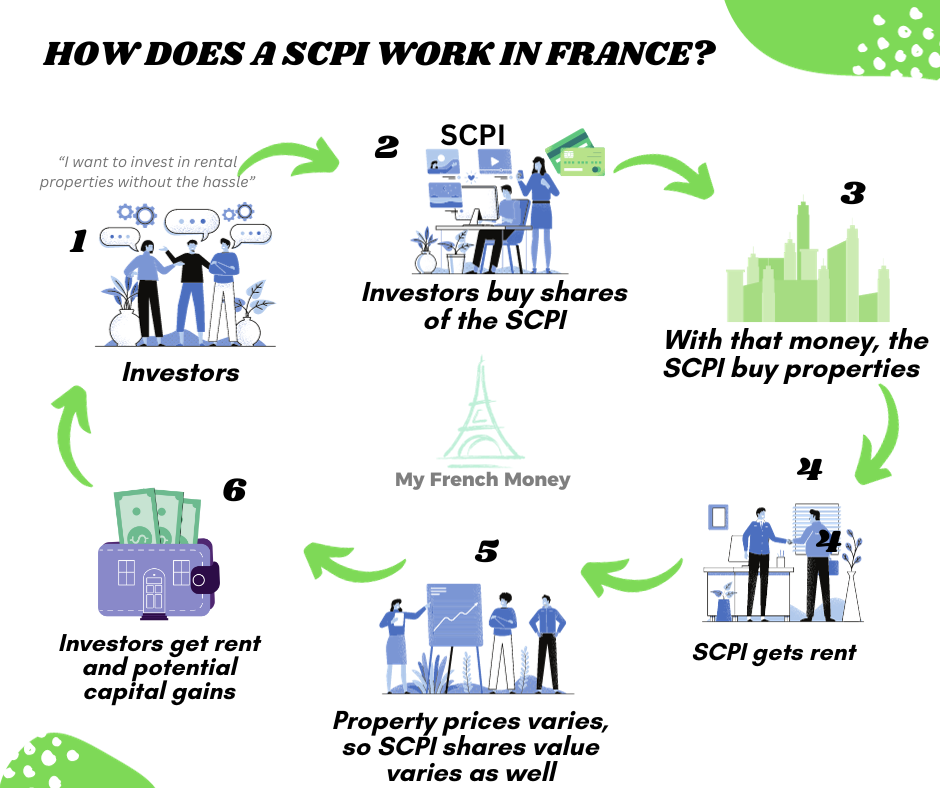

What is SCPI in France?

SCPI stands for “Société Civile de Placement Immobilier,” also known as “Pierre Papier.” This type of investment vehicle is a private company dedicated solely to purchasing and managing real estate on behalf of its shareholders, similar to Real Estate Investment Trusts (REITs). Unlike REITs, however, SCPIs are not listed on the stock market and can only own properties. Typically, they invest in commercial, industrial, and office spaces.

SCPIs are managed by a professional team that collects the invested funds and oversees the acquisition, construction, and management of the properties. Naturally, these professionals are compensated for their expertise and services.

It’s important to note that an SCPI is distinct from an SCI, or “Société Civile Immobilière.” The latter is simply a limited company used for purchasing and owning French property, without the same investment structure or focus on managing assets on behalf of shareholders.

How do SCPIs make money?

The mechanics of SCPIs follow the same principles as any other real estate rental investment. SCPIs use your money to purchase properties, which they then rent out to tenants. The income generated from these rents is distributed to shareholders in the form of dividends, typically on a quarterly basis and prorated according to the number of shares held.

Additionally, the real estate owned by the SCPI has the potential to appreciate in value over time. Each year, an independent evaluation is conducted to assess the estimated market value of the SCPI’s properties. As a result, the value of your shares may increase (or decrease) based on these evaluations.

Moreover, if a property is sold and realizes capital gains, these gains can also be distributed to SCPI shareholders as an extraordinary dividend, providing an additional benefit to investors.

What are the benefits and constraints of a SCPI?

Benefits:

- Attractive Return Rate: SCPIs typically offer a good return rate, averaging around 4.5% (in 2023), making them an appealing investment option.

- Effortless and Passive Income: Investing in SCPIs allows you to earn passive income without the hassles of property management. The SCPI handles all aspects of property acquisition and management for you.

- Good Visibility and Limited Volatility: SCPIs provide transparency regarding their investments and performance, offering a level of stability and predictability compared to other investment vehicles.

- Shared Risk: By co-owning multiple properties, you spread your risk across various assets, reducing the impact of any single property’s performance on your overall investment.

- Regular Payments: Investors can enjoy regular income distributions, typically made on a monthly or quarterly basis, providing a consistent cash flow.

Constraints:

- High Taxes and Fees: Investors may face significant taxes on income and capital gains, as well as management fees associated with the SCPI, which can eat into overall returns.

- Long-Term Investment Horizon: SCPIs are generally considered long-term investments, with a recommended holding period of eight years or more. This may not suit investors looking for short-term gains.

- Risk of Share Devaluation: The value of your shares can fluctuate based on market conditions and the performance of the underlying properties, potentially leading to a decrease in value.

- Lack of Liquidity: Investments in SCPIs are not liquid, meaning that it may be challenging to quickly sell your shares or access your capital, particularly in a market downturn.

Our tips to get the most from a SCPI in France

Invest in an european SCPI

In order to reduce taxes, it could be wise to invest in an European SCPI, as it will be taxed in the country of origin (ex: Germany) and it could represent a substantial saving compared to France... plus the diversification. However, tax return declaration becomes a little more complex.

Invest in a young SCPI

Investing in a newly opened SCPI could be a good idea, as they will invest the collected capital acquiring new properties. If they do their job right and select good ones, those properties could increase value over time (and your part's valuation as well). Today's constraints and opportunities are different (remote work, environmental requirements, etc.) and new SCPI can take advantage of that (compared to old one's that already have properties).

Invest in SCPI 'démembrée'

If you do not need the dividends right away and could wait for 5 years or more, you could buy a SCPI 'démembrée' or 'nue-propriété', which means that you will get an interesting discount on the share price but in the other hand you will give up the dividends during a given period of time. The longer, the higher the discount. For example, for a 10 year holding period, you could get up to 35% discount on the SCPI part. In addition, you do not own any taxes during this period.

Invest in SCPI with a bank loan

If you still have some credit capacity (less than 1/3 of your income), then you could request a credit to your bank to buy SCPI. It could be a good financial idea as long as the real estate interest rate (ex.: 3% with insurance included) is lower than SCPI net return (ex.: 4%). Then, the delta (1%) could be a nice leverage for you. Of course, past returns do not represent future returns. It is still a risk you will need to evaluate.

Invest with your 'Assurance Vie'

Last tip would be to include the SCPI within your ‘Assurance Vie‘ to benefit from tax exemptions associated with this investment wrapper. This can enhance your overall returns and provide additional tax advantages.

Risks of investing in a French SCPI

Investing in a SCPI carries risks, and it’s important to understand that the capital you invest is not guaranteed. In the unlikely event that the SCPI were to fail, there is a possibility of losing your entire investment. However, the likelihood of such a scenario is relatively low compared to other investment types, such as startups or stocks. Even in the case of a failure, you may be able to recover a portion of your capital, as the investments are backed by tangible assets like buildings and real estate.

Additionally, dividends from SCPIs are not guaranteed. This means your returns can vary from year to year, depending on the performance of the properties and the management of the SCPI.

The most probable risk you may face is share devaluation. By law, SCPI companies are required to conduct independent asset valuations annually. If the valuation of the underlying properties decreases, the value of your shares will likely decrease as well. The valuation of SCPIs is closely linked to interest rates and the overall real estate market, making it essential to monitor these factors when considering your investment.

How to choose a SCPI in France?

Here some points to consider when evaluating a SCPI

- Returns history. Even though good past returns does not necessarily mean good future returns, you have better probabilities to get similar ones as it is quite stable.

- Potential part revaluation. As the previous point, it is important to look at the SPCI historic revaluations and compare it against inflation rate. It is important to understand any future potential revaluation as well (ex: Better exchange rate for properties ex-Euro, emergence of a specific real estate sector like Data Centers, etc.)

- Fees. Most of the SCPI entry fees are around 8 to 12%. Then you have annual maintenance fees around 10% of total rents.

- Diversification. Unless you have a sector preference (ex.: Health) you may want to choose a well diversified one (Office, Health, Commerce, Hotels, Residential…). Some SCPI have managed to go well through COVID crisis thanks to this diversification.

- Debt rate. High interest rate environment could put stress on some SCPI.

- Flexibility to allow you to invest through an ‘Assurance Vie’ and/or with credit.

- Total valuation and years in the market.

- Cash reserves (‘report a nouveau’). It is internal savings to face potential income issues or to profit from market opportunities to acquire new properties.

- Financial occupation rate. It could be interesting to check if their properties are actually rented and generating revenue. A good rate is considered above 90%.

What are the best SCPIs to invest in France?

Here a short list of some well known SCPIs in France that are frequently listed in specialized financial magazines:

- Corum : more than 10 years returning 6-7%. It is well diversified across sectors and countries. This is our preferred one as we like their value strategy, diversification and exceptional dividends payout. If you like them as well, you may want to check our good deals page for a referral.

- Altixia Commerces (5,3% dividend in 2023) – specialized in Commercial buildings.

- Pierval Santé (5,3% dividend in 2022) – specialized in Health sector

- Iroko Zen (7,1% dividend 2023)

- Transitions Europe (8,2% in 2023)

- Remake live (7,7% dividend 2023)

Important note: This is not financial advice. Do your own research. You can lose capital invested. Past returns do not imply future returns.

Our experience with SCPI in France

In 2019, we incorporated SCPI into our investment portfolio as a hedge against inflation and a stable source of passive income. However, we realized that we made a mistake by investing outside of our ‘Assurance Vie,’ which would have provided us with valuable tax advantages. Additionally, we overlooked the opportunity to invest in a ‘démembrée’ option, which could have offered further benefits in the long term.

We allocated only a small percentage of our portfolio to SCPIs because we were unable to secure a bank credit for our preferred options, such as Corum – Origin and Eurion. Despite this limitation, we are pleased with the passive monthly dividends we receive monthly, which we automatically reinvest. This strategy aims to create a snowball effect, allowing our investment to grow over time. Overall, we appreciate the role that SCPIs play in our investment strategy, providing both stability and potential for future growth.

Last words

If you found this blog useful, please share it with friends and follow us in LinkedIn to receive more free and useful content like this. You can leave your comments below or contact us in case of any further questions.

Discover the ultimate guide to managing your money in France with our guidebook “Personal Finance in France” and unlock the secrets to thriving financially while living in France.

Bon chance!

Disclaimer

Please remember that we are not financial advisors. We are just sharing our best understanding based on our own experience. This blog is for educational purposes only. Do not make investment decisions solely based on what you read in this blog. What works for us, may not for you. Do your own research and look for professional service if required. Read our full disclaimer in the ‘about’ page.